Why You Should Consider Investing in RBI Retail Direct Bonds

Are you tired of watching your investments fluctuate with the stock market? Want to invest in something safe and guaranteed? Look no further than RBI Retail Direct Bonds. With a fixed interest rate and backed by the government, these bonds offer investors peace of mind and steady returns.

In this blog post, we'll discuss why investing in RBI Retail Direct Bonds is an excellent choice for those looking for guaranteed returns on their investment. So sit back, relax, and let us show you how to make your money work harder for you!

What are RBI Retail Direct Bonds?

The RBI Retail Direct Bonds are a new type of savings bond that is being offered by the Reserve Bank of India. These bonds are similar to the traditional government bonds, but they offer a higher interest rate and are backed by the full faith and credit of the Government of India.

The RBI Retail Direct Bonds are available in two different denominations: Rs. 10,000 and Rs. 1 lakh. The bonds will mature in 7 years, and will pay interest at the rate of 7.75% per annum (compounded annually).

Benefits of Investing in RBI Retail Direct Bonds

When it comes to guaranteed returns, few investment options can match the RBI Retail Direct Bond. RBI Retail Direct Bonds are issued by the Reserve Bank of India and are backed by the full faith and credit of the Indian government.

The bonds offer a fixed rate of interest for the life of the bond, and are payable semi-annually. RBI Retail Direct Bonds are an excellent investment option for risk-averse investors who are looking for guaranteed returns.

The RBI Retail Direct Bond offers several benefits that make it an attractive investment option:

• Guaranteed Returns: The RBI Retail Direct Bond offers a fixed rate of interest that is paid semi-annually. This makes it an ideal investment for risk-averse investors who are looking for guaranteed returns.

• Safety: The RBI Retail Direct Bond is backed by the full faith and credit of the Indian government, making it one of the safest investment options available.

• Flexibility: The bonds can be held for any length of time, from one year up to 10 years. This gives investors the flexibility to choose an investment horizon that suits their needs.

• Liquidity: The bonds can be redeemed at any time after they are issued. This makes them highly liquid, which is ideal for investors who may need to access their funds at short notice.

How to Apply for the Bonds

RBI has announced the launch of Retail Direct Bonds, which will offer guaranteed returns to investors. The bonds will be issued through a public offer, and interested investors can apply for them online.

The application process is simple and straightforward. Investors need to log on to the RBI website and fill in the online application form. They will then need to submit the form, along with KYC documents and a cheque for the desired amount.

Once the application is received, RBI will process it and issue the bonds within 15 days. The bonds will be credited to the investor's account, and interest will be paid out on a quarterly basis.

Investors can choose to receive their interest payments either through direct credit into their bank account or through physical cheques. Interest payments will start from the date of issuance of the bonds.

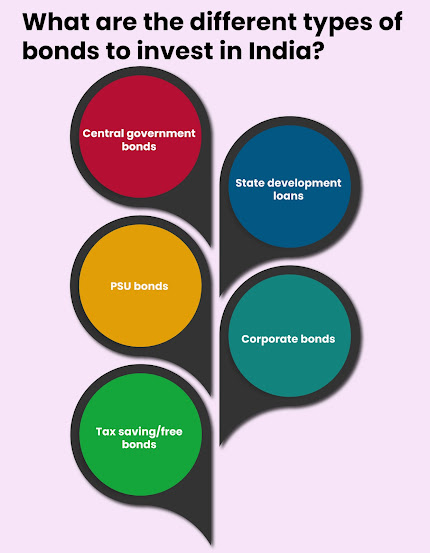

Types of Bonds Available

The Reserve Bank of India (RBI) offers a variety of bonds for retail investors. The interest rates on these bonds are guaranteed, making them a safe and secure investment option.

The RBI offers three types of retail bonds: government securities (G-Secs), treasury bills (T-Bills), and corporate bonds. G-Secs are the safest investment option, as they are backed by the Indian government.

T-Bills are also backed by the government, but they have a shorter maturity period than G-Secs. Corporate bonds are issued by companies and carry more risk than G-Secs or T-Bills, but they often offer higher interest rates.

Investors can purchase RBI retail bonds through banks, brokerages, or the RBI itself. The minimum investment amount is Rs 10,000 for G-Secs and T-Bills, and Rs 1 lakh for corporate bonds. Interest payments are made semi-annually, and bonds can be held to maturity or sold prior to maturity.

Risk Factors Associated with Investing in RBI Retail Direct Bonds

There are several risk factors associated with investing in RBI Retail Direct Bonds, including:

-Investor risk tolerance: RBI Retail Direct Bonds may not be suitable for all investors. Those who are more risk-averse may prefer to invest in other types of bonds or securities.

-Market conditions: The performance of RBI Retail Direct Bonds is directly linked to the general condition of the bond market. When interest rates rise, the value of bonds typically falls.

-Credit risk: There is always the possibility that the issuer of the bond will default on its payments. This risk is higher for bonds with lower credit ratings.

-Liquidity risk: RBI Retail Direct Bonds may be difficult to sell before maturity, especially if market conditions are unfavorable.

How to Manage Your Investment in RBI Retail Direct Bonds

When you invest in RBI Retail Direct Bonds, you are guaranteed to receive a fixed return on your investment. However, there are some things you need to do in order to ensure that your investment is managed properly and that you get the most out of it.

Here are some tips on how to manage your investment in RBI Retail Direct Bonds:

1. Monitor your bonds regularly. Keep track of the performance of your bonds and make sure that they are meeting your expectations. If not, consider selling them and reinvesting the proceeds into another bond issue.

2. Review your bond portfolio periodically. As your needs change, so too should your investment strategy. Review your bond portfolio at least once a year to ensure that it still meets your goals and objectives.

3. Diversify your bond holdings. Don't put all of your eggs in one basket by investing only in RBI Retail Direct Bonds. Consider investing in other types of bonds as well, such as corporate bonds or government bonds. This will help reduce risk and improve returns over the long term.

4. Stay invested for the long term. Bond prices fluctuate, but over time they tend to go up in value. Therefore, it's important to stay invested for the long term in order to maximize returns.

Conclusion

Investing in RBI Retail Direct Bonds is a smart and secure way to ensure a steady stream of income through guaranteed returns. It offers the added advantage of flexibility that allows you to tailor your investment portfolio according to your own financial goals. With its low-risk nature, this investment option can provide you with long-term stability if managed properly. Therefore, it is definitely worth considering for those who are looking for an assured return on their investments without any hassles or complications. For More information you can visit Bondsindia (OBPP).

Comments

Post a Comment